Tips for Saving Money

By NFIU

Article No. : 01/2020

In today’s day and age, we have a lot of expenses with some known and many unforeseen. Medical emergencies in the family, funeral expenses, and loss of property due to floods or fire are all but a few of the reasons why spending a lot of money is the cycle of life for many. Most times people end up borrowing for meeting their expenses. Every new year we have some common expenses such as school fees; cost of exercise books, uniform and stationery for children going to schools. The start of the school year is a big expense and of course during December, many families spend money for Christmas. Besides those major expenses, all families have also those regular or daily expenses like food, transport, clothing and so forth.

With every family in Solomon Islands having both planned and unplanned expenses, it is therefore important that we learn how to save money, for both of these types of expenses. It is better to save for these expenses instead of having to borrow money to pay for them, as unplanned expenses. Having regular savings, even small amounts (say $2 per day) will help us to lessen some of these hardships of life. It will give us the much-needed cushion to absorb shocks caused by emergencies or unplanned situations.

The first few steps to take in order to save, is to have a simple financial plan for the family. One can have short term, medium term and long term savings goals as described below:

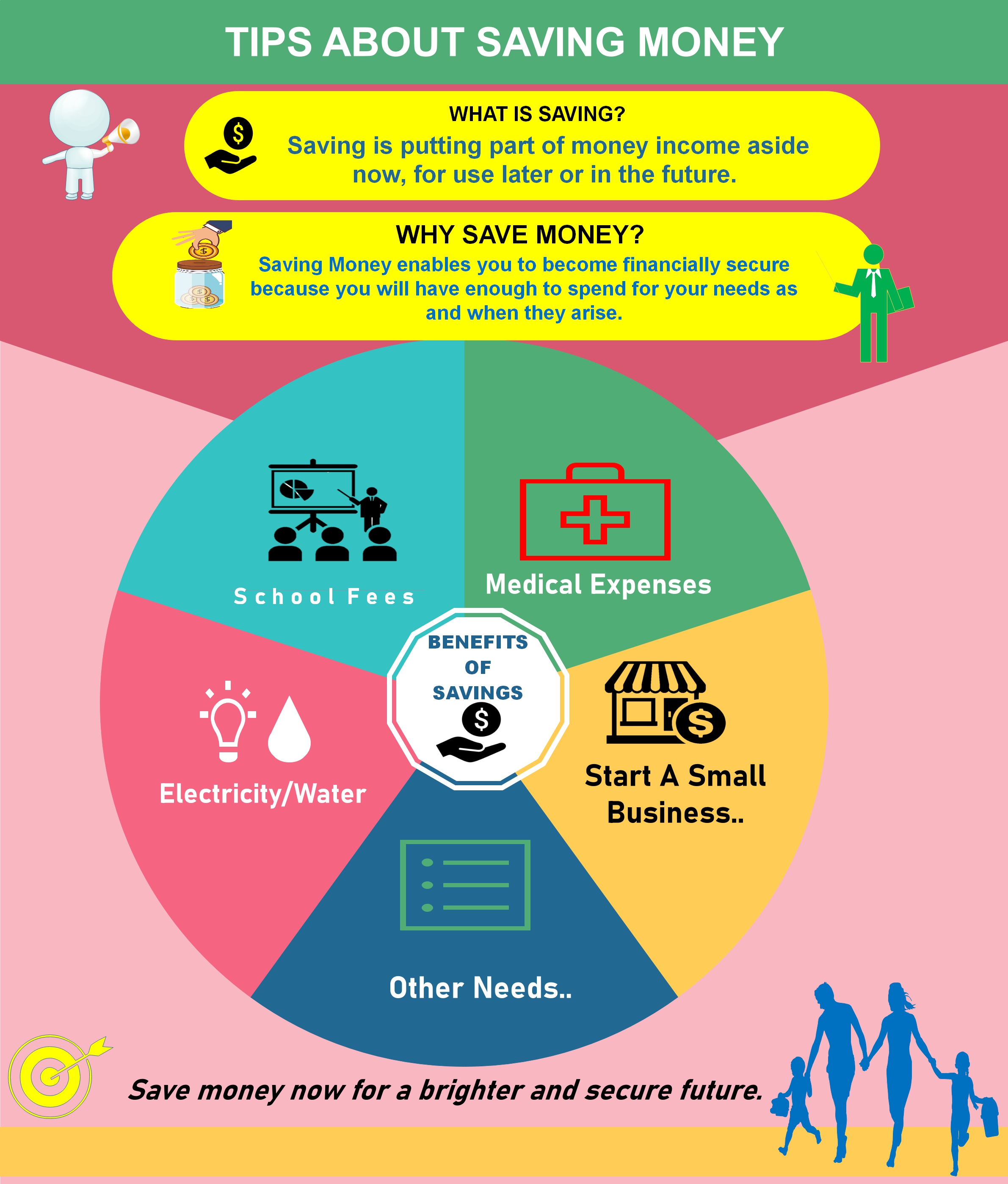

Short term (up to one year): To meet both planned and unplanned expenses. School fees, medical expenses, social obligations, church obligations are examples.

Medium Term (over one year and up to 5 years): These are to meet expenses like a planned overseas travel, education of children abroad, buying a car or repairs to our house, buying household utilities (eg: DVD, TV, fridge etc.)

Long Term (above 5 years): Long term savings goals are mainly for old age, retirement, building a new house and leading a peaceful life after retirement.

It is important for every family and household in Solomon Islands to start thinking about Savings for the future and develop simple savings plans adapted to their conditions, suitable to their needs and one that they are capable of implementing.

How you can save your money

In most villages the use of money (banknotes and coins) is still limited and most of the daily needs such as food are usually readily available such as vegetables, fruits, fish and root crops. However money or cash is still required to meet other needs like buying rice, bread, fuel, paying school fees and so forth. Therefore, in most of our villages, people tend to keep their money or cash under mattresses, in pots, in tins, wooden boxes and sometimes in floats. However this is not safe and the money can be lost due to fire, floods or theft.

So, how can people keep their money safely? Listed below are some ways of keeping your money safe and saving it.

Banks: Banks are commercial financial institutions working under the supervision of the Central Bank and following rules, regulations and procedures laid down by the relevant laws. Banks offer products and services that encourage people to save money and keep their savings secure for a future use. Let us now see some simple savings products that banks offer.

Savings Account: All banks now offer simple savings accounts that allow individuals to put away small sums of money at regular intervals and draw the money when they need it. Savings account can be opened through any of the bank branches or agencies. Also now with the introduction of mobile and branchless banking in the Solomon Islands, savings accounts can also be opened through bank agents. Banks also provide an electronic card that can be used in an ATM or an EFTPOS terminal to transact. While there are no fees for depositing money, usually there is a small fee for withdrawals. A bank savings account while being the simplest form of savings is one of the most secure as all customer deposits with a bank are fully protected. However, savings accounts in the Solomon Islands do not carry any interest. For short term and immediate savings, Solomon Post also provides Ezi-pei where you can save by cashing in to your Ezi-Pei wallet and used it to Pay bills or P2P transfers when the need arises.

Term Deposits: Term deposits also called fixed deposits are another form of savings provided by banks. Term deposits are usually for a fixed term (say one year, two years etc.) and carry a small interest. Usually banks accept term deposits for lump sum amounts (eg: $2000, $5000 etc.). For people with large amounts of cash, term deposits are a good way of saving for a medium term and also earning an interest on their savings.

Solomon Islands National Provident Fund: The SINPF is the only provider of super annuation benefits in the country. Individuals can become members of NPF either by contributing savings through their employers or directly as voluntary members. For those employed, NPF membership is mandatory or compulsory. Member contribution is 7.5% of gross wages and employer contribution is 5% and total is 12.5%. NPF is a good route for saving money for long periods and building a fund for retirement and old age. For the informal sector, they can now save with SINPF YouSave.

SINPF YouSave :YouSave is a pension savings scheme design purposely for the informal sector segments such as taxis and bus drivers, vegetable and betel nut market vendors, fishermen, students, house wives among others. YouSave have two accounts – (1) Preserved account – members can withdraw savings after 55 years (2) General account – Members can withdraw their savings at anytime but only 4 times a year. Every deposit a member makes is split 50-50 between their General and Preserved account. Members who register with youSave gets the same percentage of returns received by the formal sector. YouSave also provides a channel that enable members to deposit to their youSave accounts using Mobile top-ups from their phones.

Credit Unions: Credit Unions are cooperative institutions, with voluntary membership and democratically managed by members through their elected representatives. Credit unions provide services such as savings and loans. In many countries credit unions have proved to be very useful in providing a range of savings services appropriate to the needs of their members, besides good returns in the form of dividends to members. In the Solomon Islands, there were over 200 credit unions in the 1990s including several in rural areas. Presently there are only around 17 functioning credit unions with most of them being employee based ones based in Honiara.

Savings Clubs: Savings clubs, unique to the Solomon Islands, are rural financial enterprises that operate in communities that have no access to banking services. Typically a savings club consists of 20 to 25 members who meet regularly, say once a week or a fortnight, save small amounts and use the savings to pay school fees, emergency medical expenses, starting a small business etc. Savings clubs provide the basic financial services in a village and are run by the members themselves. Savings clubs are a very useful form of financial intermediation in the rural areas, where access to other formal financial services is lacking.

Issued by the Consumer Empowerment Working Group (CEWG)

National Financial Inclusion Task force (NFIT)

Central Bank of Solomon Islands

{kind=link}

{kind=link}